Using Capital Gains to Pay for College

Background

If paying for college were a joke, the laughter would seem like a Jerry Seinfeld comedy routine. Unfortunately, paying for college is no joke. Regardless of one's views on the exorbitant arc college tuition has carved over the past generation, the bottom line is this: a college degree is a near-requisite voucher to reasonable compensation. True, exceptions to this supposition exist, though that species is rare. For better or worse, more people than ever are pursuing higher education.

College Funding is its own "cottage" industry. You can save in an Education Savings Account ESA, or Coverdell), a Uniform Transfer to Minors Account (UTMA, or a UGMA in some states), or a 529 Plan just to name a few. Additionally, there is a cornucopia of helpers to assist with figuring out how to get to that diploma.

For some, college savings begins on the way home from the hospital in the days after child birth. For others, the schedule is a bit more stretched out, or - UGH, non-existent. Whatever the college savings situation, there are three critical components to paying for college:

- The amount of assets available to pay for college

- The location of the assets, ie the type of account in which the funds reside

- The college the student will attend, and more importantly, how the final college expenses are calculated

Using an Education Savings Account or 529 Funds isfairly straight-forward. A much less well-publicized strategy involves using the Parents' own taxable brokerage account assets to pay for school - that is the subject of today's article.

If you prefer to watch an explanation of this strategy, check out our video:

Taxable Brokerage Accounts

For most people, personal savings begin with their employer-sponsored plan. Once that bucket tops out, Individual Retirement Accounts (IRAs) are a frequent second act, and then a regular Taxable Brokerage Account may be next in line.

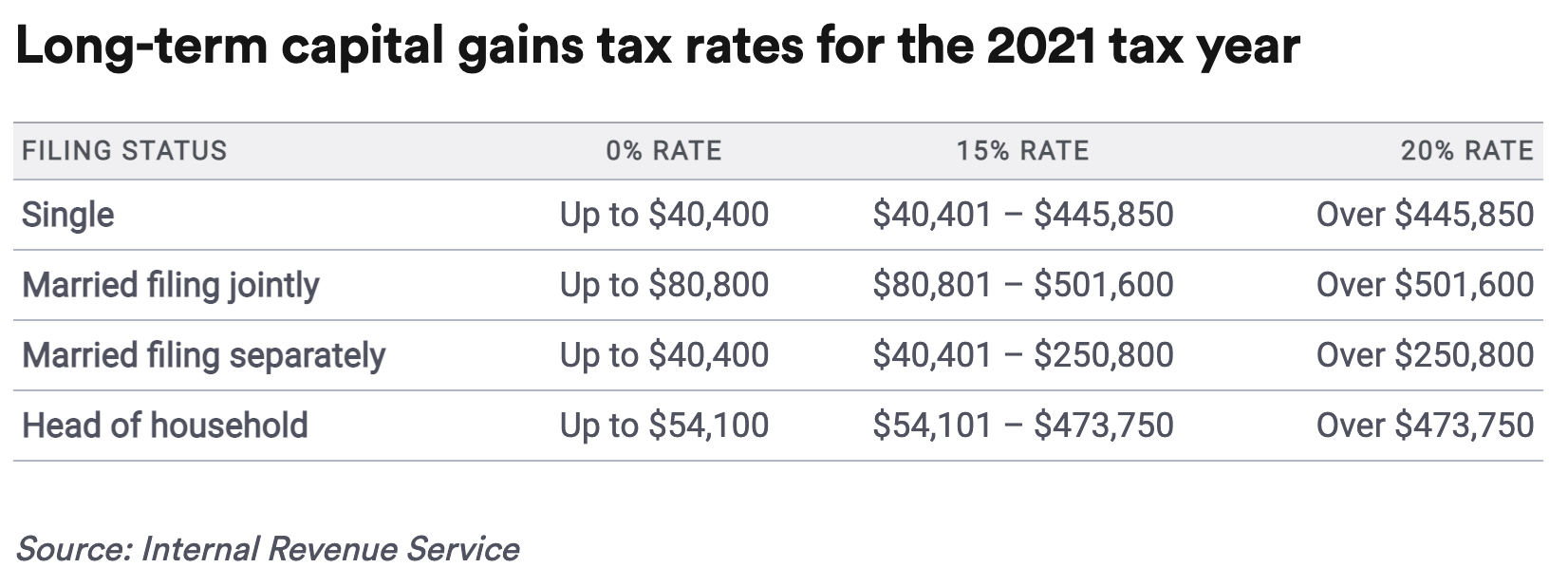

Given that employer-sponsored plans and IRAs have no income tax consequences for Capital Gains, Investors can safely ignore Capital Gains Taxes in those accounts. For taxable accounts, conversely, Capital Gains are a major consideration. Short-Terms Gains - proceeds from the sale of assets held less than one year - are taxed as regular income. Depending on one's income, Long-Term Capital Gains Taxes can range from 0% up to 23.8% at the Federal Level. The chart below describes the first level of Capital Gains Taxes.

The second level - the "Medicare Surcharge" an equals 3.8% and applies to certain individuals at the 20% Long-Term Capital Gains Rate. And then for those whose states have them, Investors also have to consider those pesky State Income Taxes as well.

Some Academics

Before we go on, it is important that you understand a few financial concepts:

1) The American Opportunity Tax Credit

The American Opportunity Tax Credit (AOTC) is an Income Tax Credit provided during the first four (4) years of higher education. As opposed to an Income Tax Deductions, which reduces your taxable income, a Tax Credit directly decreases your Income Taxes due - a much better benefit.

Those claiming this credit receive a maximum annual credit of $2,500 per eligible student. To earn the entire credit, a minimum a $4,000 of college expenses are needed. The first $2,000 of expenses receive a dollar-for dollar credit. For expenses above $2,000, the crediting rate is 25% up to the $2,500 limit of the tax credit. More simply put, the first $2,000 yields a $2,000 credit and you need $2,000 more of expenses to maximize the credit. For those in the know, it is exceedingly simple to generate $4,000 of college expenses.

If the credit brings the amount of tax you owe to zero, you can have 40 percent of any remaining amount of the credit (up to $1,000) refunded to you. Another significant benefit to this credit.

There are income limitations to claiming the AOTC. For single filers, the Tax Credit begins phasing out at $80,000 of Adjusted Gross Income and is no available at $90,000 of AGI. The brackets are double for married filers, ie $160,000 and $180,000.

2) Claiming a Child as a Dependent

Most parents are somewhat familiar with the rules governing claiming a Child as a dependent. For a refresher, here is a brief, NOT EXHAUSTIVE, list of criteria:

Relation.

The child can be your son, daughter, stepchild, eligible foster child, brother, sister, half brother, half sister, stepbrother, stepsister, adopted child or an offspring of any of them.

Age.

Do they meet the age requirement? Your child must be under age 19 or, if a full-time student, under age 24. There is no age limit if your child is permanently and totally disabled.

Residence.

Do they live with you? Your child must live with you for more than half the year, but several exceptions apply.

Financial Support.

Do you financially support them? Your child may have a job, but that job cannot provide more than half of her support.

For most of a Child's early years, these criteria are easily met. Upon entering the College Years, this changes the nature of the game significantly. We will utilize this factor later on - you'll see.

3) The "Kiddie Tax"

The "Kiddie Tax" was designed to prevent high-earning and/or High Net Worth individuals from funneling assets and income to their children to avoid Income Taxes. Essentially, when large amounts of income are transferred to Minors, the income is treated as if it were the Parents' own income, thus negating the tax benefit of the transfer. The concept has experienced several iterations over the years. As of 2021, the criteria for paying the "Kiddie Tax" are as follows:

(i) The child's unearned income was more than $2,200.

(ii) The child meets one of the following age requirements:

a. The child was under age 18 at the end of the tax year,

b. The child was age 18 at the end of the tax year and you didn't have earned income that was more than half of the child's support, or

c. The child was a full-time student at least age 19 and under age 24 at the end of the tax year and the child didn't have earned income that was more than half of your support.

(iii) At least one of the child's parents was alive at the end of the tax year.

(iv) The child is required to file a tax return for the tax year.

(v) The child does not file a joint return for the tax year.

There are A LOT of nuances to the "Kiddie Tax". As a very rough rule of thumb, almost all College Students will be subject to it. Almost here means that there are exceptions and you definitely will want to consult a tax advisor in all cases. For the purposes of this article, however, we will assume all College-aged Students are subject to this tax.

Using Capital Gains to Pay for College

The Uniformed Transfer to Minors Account is a very, very flexible tool for those Investors with a lot of assets. At the lowest levels of investment income, an Investor can achieve a 0% Tax Rate on Capital Gains and Income - I wrote about that strategy here.

As children enter college, another strategy opens up to parents - and this is one ALL Parents with large Capital Gains and AGIs over $160,000 should consider. This strategy utilizes the American Opportunity Tax Credit (AOTC) and the IRS's Dependency and "Kiddie Tax" Rules described above.

When a Child receives assets into a UTMA Account, this transfer represents a completed gift. While the Child does have a "Custodian" for the account, the assets residing in the account are the Child's property and must be used for the child's. College Tuition certainly qualifies.

The basic strategy here involves transferring appreciated assets to the Child. Then, entering the College Years, the Tuition, Ancillary Expenses, and residing away from home will collectively push the Child out of the "Dependent" Status described above. However, the Child will meet one of the "Kiddie Tax" criteria also described above.

Here is a graph depicting the anatomy of an Asset Transfer to a Minor:

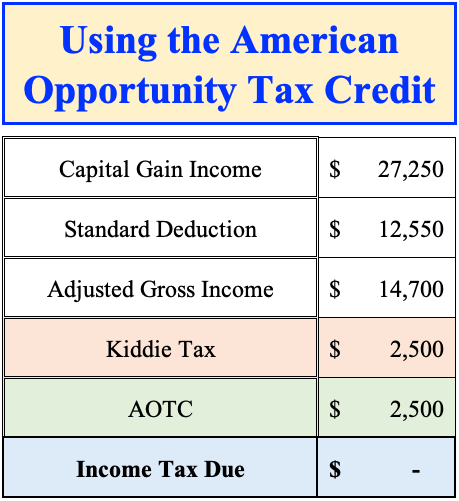

As with an asset sale, we have to consider the Income Tax implications. For starters, working with the Minor, Parents will collect the IRS Form 1098-T showing the amount of College Expenses incurred and then have a tax return prepared for the Child. I have chosen to illustrate the maximum Capital Gains Tax avoidance. The outcome is still beneficial for Capital Gains of lesser amounts. Effectively, the math works as follows:

For Single Filers, which is what the Minor is in this example, the Capital Gains Tax Rate is 0% up to $40,000 of Capital Gains. However, since the Child is between 19-24 AND a College Student (See the "Kiddie Tax" Criteria above), the Capital Gains are taxed using the "Kiddie Tax" rules. Happily, the American Opportunity Tax Credit satisfies the Income Taxes owed, thus resulting in an exceptionally efficient way to offset College Expenses. I have saved all the associated tax forms to simplify the presentation. However, before pursuing this strategy, it is strongly advised to consult your Income Tax Preparer and ask him/her to prepare a sample Income Tax Return showing the $0 balance due.

Benefits of Using Capital Gains to Pay for College

1) Capital Gains Tax Avoidance for the Parents

Avoiding 23.8% in taxes is interesting to most people. Moreover, when it is done in pursuit of a child's college education, even better! Give that the current Bull Market has likely resulted in rather large capital gains for Investors. Transferring Appreciated Assets to Minor Children in lieu of simply giving cash can be a wise choice.

2) Utilizing the American Opportunity Tax Credit

Since the American Opportunity Tax Credit phases out for some, it is advisable to look at strategies to still utilize it. Maneuvering Appreciate Assets is such a strategy.

3) Eliminating Appreciated Assets from your Portfolio You no longer want to hold

For some Investors, the investment they purchased a 'X' not as attractive at '3X'. However, the same Investor may be loathe to pay Income Taxes on the Capital Gains. Therefore, transferring the asset to a Minor Child may make a lot of sense for that same Investor.

4) Preserve existing College Savings

For some - like my Grandparents - education is extremely important. For Parents of means, they may want to utilize their Appreciated Taxable Assets currently in order to preserve existing college savings - think 529s or Coverdells - for other children, graduate school, grandchildren, or even - gulp - themselves.

Who Should Use This Strategy

1) High Earners

For those with an Adjusted Gross Income of over $80,000 (Single) of $160,000 (Married), the American Opportunity Tax Credit (AOTC) should be a strong consideration. Its use may have an impact on grant and scholarship awards at a given school, so you should be mindful of the impacts of this strategy before employing it. Your Child's College Financial Aid office will be an invaluable resource before pulling the trigger an Asset Transfers.

2) Those with Large Taxable Holdings and Significant Capital Gains

If you have large Capital Gains in a Taxable Account, it is well-worth your time and effort to explore the best uses of appreciated stock. Selling stocks and paying the full 23.8% freight on the sale should be a last resort...there are many strategies to consider to avoid the full impact. A Financial Planner specializing in this area could be of use to you for such an endeavor.

3) Aggressive College Savers

If you are saving multiple thousands of dollars per month into a 529 - the preferred College Savings vehicle - the contributions in the last 1-3 years will most likely find their way to a "cash preservation" fund within the 529 Plan. Since most plans have an age-based strategy, most of the funds will be moving from equities to more stable value assets, which are much less volatile. Therefore, the investment results for a stable value investments will be similar in either a 529 or a simple taxable account. Therefore, it may make more sense to preserve cash in your own taxable account, which is more flexible for use than a 529.

4) Late Starters on a College Savings Plan

If college savings were not a priority in your early years and it is only recently that you've put your foot on the gas, the typical college savings vehicles - think 529s - will not be as beneficial to you because you are missing out on a great deal of compounding time. So, if you for some reason have large Capital Gains AND are aggressively saving for College, then this strategy may make a lot of sense for you. Partnering with a Financial Planner to assist you through this process may be something for you to consider.

Conclusion

Funding a College Education has morphed into a seriously complicated problem. And to make it even more interesting, the bills keeping growing and growing with seemingly no end in sight. Among other strategies, utilizing Capital Gains may be a tremendous benefit for some. I encourage you to consider it for your own College funding needs.

We’re Here to Help

Paying for College is a stressful endeavor for ALL Parents...if you are feeling it, you are definitely not alone. We at Resilient Asset Management are here to help. If you'd like to talk about your specific circumstances, please schedule a 30-minute introductory meeting or contact us at chris@resilientam.com or (901) 318-3423.

About Christopher

Christopher Flis is founder and financial planner at Resilient Asset Management, a fee-only Registered Investment Advisor (RIA) based in Tennessee. Chris graduated from the United States Naval Academy with a bachelor’s degree in computer science, earned a Master of Science in Computer Science from the University of Minnesota, and attended flight school in Pensacola, FL, launching a fulfilling and distinguished military career. Chris spent 20 years in the Navy as an F/A-18 Strike Fighter Pilot, which included tours in Japan, Australia, and California, combat missions in all areas of the Persian Gulf and Afghanistan, and time spent as the Executive Officer of Naval Base Guam and Director of Navy Casualty in Millington, TN. When Christopher was ready to make a career change, he turned to a passion he held since high school when he attended a lecture on personal finance and started managing his own investments. He earned his Certified Financial PlannerTM (CFP®) designation and now combines his passions and experience by serving military, retired military, business owners, and retirees. Chris provides comprehensive, customized financial services, helping his clients overcome their challenges and take opportunities so they can achieve financial independence.

Chris lives in Downtown Memphis with his wife, Christine, and his son, Emerson. He is an avid runner and when he is not jogging for exercise, he is usually chasing his son around or walking his 3 dogs. To learn more about Chris, connect with him on LinkedIn.