You’re a 22% Taxpayer for Life

Most military members are told to defer taxes now and pay less later. But for career service members under the legacy High-3 system, that logic breaks down. Here's why the Roth TSP is the smarter default — and what the numbers actually show.

MILITARY RETIREMENTRETIREMENTTAXES

Christopher Flis

6/25/20268 min read

Note: This analysis applies to service members under the legacy High-3 retirement system only. If you joined on or after January 1, 2018, or opted into the Blended Retirement System (BRS), this article does not reflect your situation.

If you’ve spent any time around financial advice, you know the gospel of tax deferral by heart. Put money in pre-tax while you’re earning well and sitting in a high bracket, then pull it out in retirement when your income (and your tax bracket) comes down. Defer high, withdraw low. Simple enough. And I’ve seen the illustrations showing that identical tax rates yield the same result at withdrawal time.

For military retirees, there are a few more curveballs in play.

That’s a strong claim, so let me show my work. Military pay is built differently than civilian pay, and a military retirement under the legacy High-3 system, while very lucrative, bends the logic of deferral quite a bit. These two differences necessitate specialized analysis. By the time we’re done, I think you’ll see why, for the typical career military member serving under the old retirement model, the Roth TSP is the savvier default.

To be sure, the traditional TSP has its place, though its use case is more nuanced than most people realize. More on that later. First things first.

One honest caveat before we dig in. I said most, not all. This article also assumes you’re serving under the legacy High-3 retirement system, meaning you joined before January 1, 2018 and did not opt into the Blended Retirement System. If you’re under BRS, the matching contributions and different pension structure change the analysis meaningfully, and this piece isn’t written for you. If your household has a second high earner, a spouse pulling a physician’s or an executive’s income, for example, or you’re wearing stars, the picture also shifts and deferral may earn its keep. But for the vast majority of military families living on a single military income under the legacy system, what follows lands squarely.

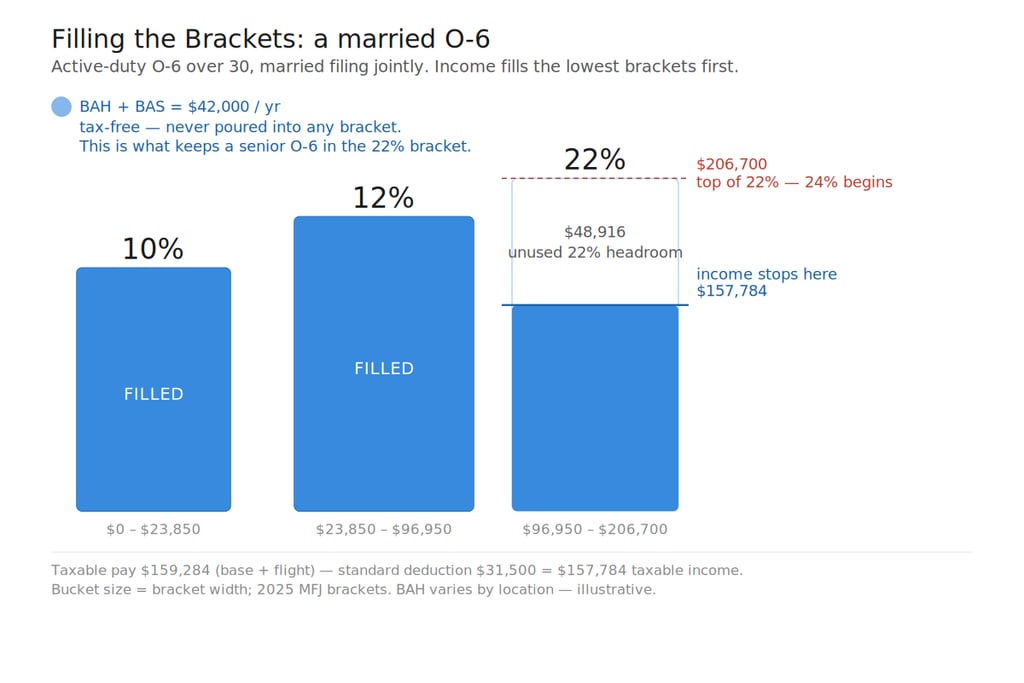

You’re a 22% Taxpayer While You Serve

Here’s the first thing that makes us different: a big chunk of our pay never shows up on a tax return at all.

Basic Allowance for Housing and Basic Allowance for Subsistence (BAH and BAS) are tax-free. Depending on where you’re stationed, that can be $40,000 a year or more of compensation the IRS simply never sees. Add COLA to that list as well. Your base pay is taxable, your flight pay is taxable, but the allowances are not.

That does something subtle and powerful: it holds your taxable income well below your total compensation, which keeps your tax bracket lower than your paycheck would suggest.

Run the numbers on a senior O-6 with 30 years drawing flight pay, one of the highest-compensated military members serving. Base pay lands around $182,000, plus taxable flight pay on top. Married, filing jointly, taking the standard deduction, that household’s taxable income comes in around $158,000 and lands squarely in the 22% bracket. Not 32%, not 24%. Twenty-two. The tax-free allowances are the reason.

So when you make a traditional TSP contribution, the tax you’re deferring is only being charged at 22 cents on the dollar to begin with. The whole appeal of deferral is dodging a high rate now to pay a lower one later. If the rate now is already low, there isn’t much of a deal to be had.

For the single officers reading this: filing single, that same O-6 crosses into the 24% bracket. The deferral case gets weaker still.

In Retirement, There Are No Low-Income Years

This is the half of the equation almost everyone misses — because it’s the half that civilians don’t have to think about.

A civilian who retires without a pension gets a stretch of genuinely low-income years: the gap between the last paycheck and the first Social Security or RMD check. In my world, we call this the “Golden Age” of financial planning — a window where tax alchemy permits the conversion of money deferred at 37% to be moved into the tax-free bucket at 10% and 12%.

For military retirees, that window simply doesn’t exist.

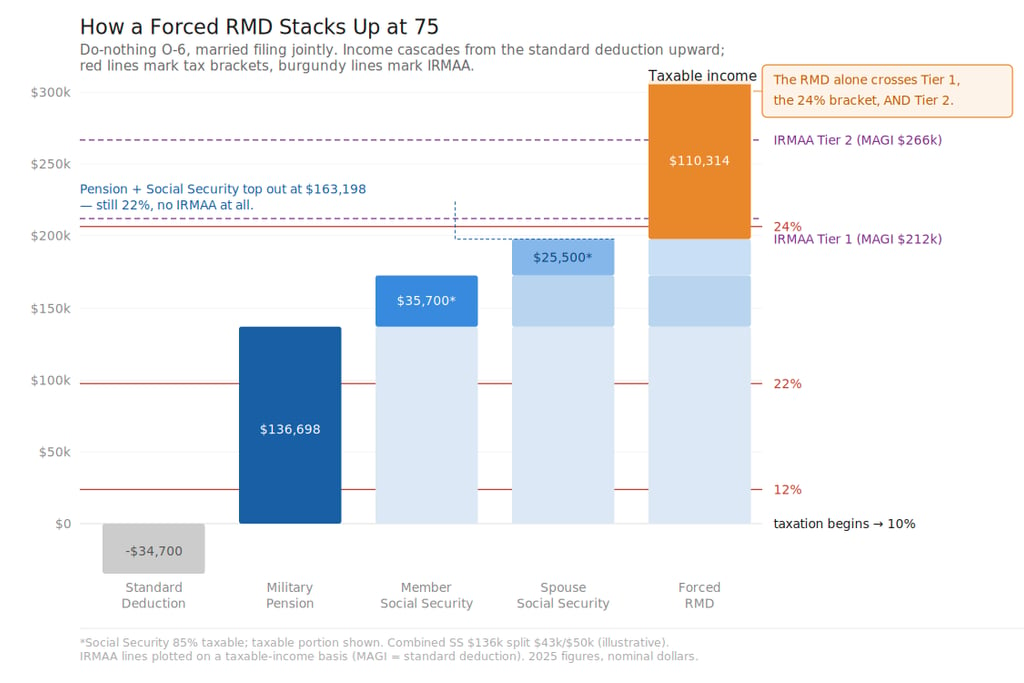

A 30-year O-6 retires with a pension somewhere around $137,000 a year — guaranteed, inflation-adjusted, and starting the month you take off the uniform. That pension alone fills the entire 10% bracket, the entire 12% bracket, and pokes into the 22%. Before Social Security. Before you’ve touched a dime of the TSP. The cheap brackets are already flooded.

Now push it to the extreme. Assume you retire at 50 with $500,000 in a traditional TSP, stop contributing, and let it compound at a reasonable rate of return. By the time Required Minimum Distributions kick in at 75, that balance has grown to roughly $2.7 million — and the IRS now forces you to start pulling it out, whether you need the money or not. That forced withdrawal stacks on top of your pension and Social Security, and the whole pile lands you solidly in the 24% bracket.

It gets worse, because of a quieter penalty called IRMAA — the income-related surcharge on your Medicare premiums. Cross certain income thresholds and your Medicare Parts B and D get more expensive, for both you and your spouse. And IRMAA is a cliff, not a ramp: one dollar over the line and you owe the full surcharge.

Look at where the damage comes from. The pension and Social Security alone top out in the 22% bracket with no IRMAA exposure at all. It’s the RMD, the money the traditional TSP forced into the open, that pushes you into 24% and over the IRMAA cliff.

So here’s the choice laid bare. You can pay 22% now, on your terms. Or you can defer, let the balance compound, and pay 24% later, by force, on the government’s schedule, with a Medicare surcharge attached. That’s not deferring high to pay low. That’s deferring low to pay high.

What Roth Does Instead

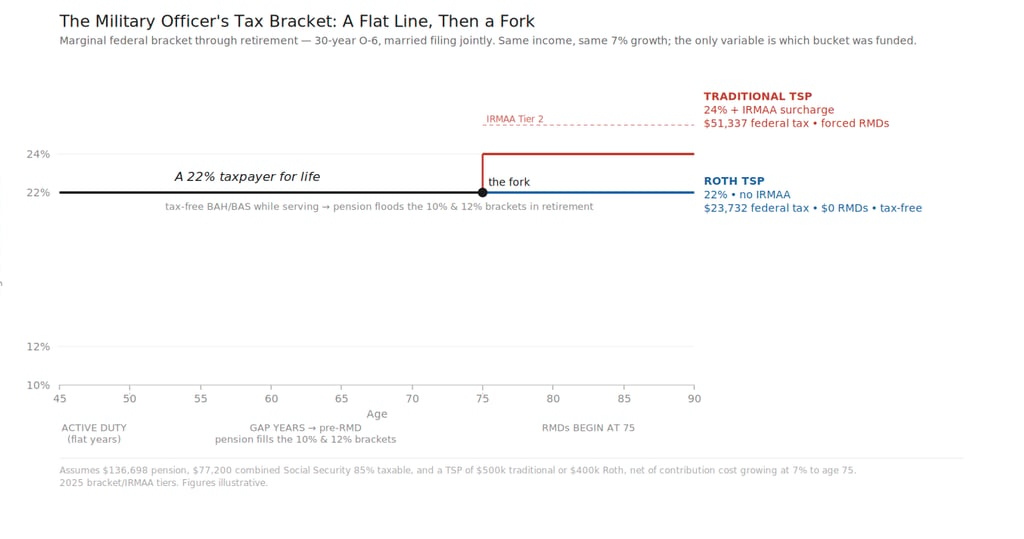

Now run the same person, same career, same rate of return, but funded into the Roth TSP instead.

Funding Roth means paying the tax on the way in, so let’s be fair and give the Roth saver a smaller starting balance to account for it, say $400,000 at retirement instead of $500,000. Same growth from there. At 75, here’s how the two stack up:

The traditional saver has the bigger statement balance — but it’s pre-tax, it triggers RMDs, and stacking those RMDs on the pension and Social Security puts them in the 24% bracket with an IRMAA surcharge.

The Roth saver has no RMDs, holds in the 22% bracket, owes no IRMAA surcharge, and pays roughly half the federal tax in retirement. Every dollar of that Roth balance is theirs to spend, tax-free, on their own timeline.

Here’s the part worth reading twice. Even though the Roth saver started with $100,000 less, they end up with more money they can actually spend. A traditional balance isn’t really yours. It’s yours minus a tax bill that’s been quietly compounding right alongside the principal for 25 years. The statement says one number; the spendable number is smaller. The Roth statement and the spendable number are the same number.

One thing I won’t oversell: the Roth doesn’t lower the tax on your Social Security in this scenario, because the pension alone is large enough to make 85% of your benefit taxable regardless. The Roth win is the lower bracket, the avoided IRMAA, and a tax-free pot with no strings attached. That’s plenty.

When Deferral Makes Sense: Charitable Giving

It would be a disservice to tell you traditional money never has a place. It does, in one spot especially, and it’s worth knowing.

If you’re charitably inclined, a Qualified Charitable Distribution (QCD) is one of the best tools in the tax code. Starting at age 70½, you can send money directly from a traditional IRA to a charity, and it counts against your RMD while being excluded from your income entirely. That’s better than a deduction, and it can pull your income back below those IRMAA thresholds. (A wrinkle worth noting: QCDs come from an IRA, not directly from the TSP, so the move is to roll a deliberately sized slice of traditional money into an IRA earmarked for giving.)

So the smart structure isn’t “all Roth, always.” It’s “Roth as the default, with a right-sized traditional sleeve if you give.”

A note on the Blended Retirement System: if you joined on or after January 1, 2018, or opted into BRS, this article is not written for your situation. The government’s matching contributions and the different pension structure under BRS require a separate analysis. The framework here applies to legacy High-3 members only.

The Bottom Line

Stack it all up and the message is simple.

You’re a 22% taxpayer while you serve. You’re still a 22% taxpayer in the retirement years before RMDs, because the pension floods the cheap brackets. And if you do nothing, you become a 24%-plus-IRMAA taxpayer at 75, because RMDs force your hand.

There is no low-income valley waiting for you. There is no cheaper rate to hold out for. You are, for all practical purposes, a 22% taxpayer for life.

When that’s the reality, the move is to stop chasing a discount that isn’t coming and instead lock in a known, fair rate. Own your retirement money outright, free of future tax-rate guesswork, free of forced withdrawals, and free of the IRMAA cliff. By any honest measure, today’s brackets are historically low. Roth lets you bank that rate and stop worrying about where rates head next.

In practice, for most service members that means three things: lean your TSP contributions toward Roth; if you’ve already built a traditional balance, look hard at converting it during your lower-income years before RMDs force the issue at a worse rate; and keep a slice of traditional money only if you intend to give it away. None of that requires perfect timing. It just requires recognizing that the usual advice was written for someone whose career looked nothing like yours.

Your TSP decision is worth a conversation.

Every military family’s numbers are different. If you’re within a few years of transition and want to run your specific scenario, including bracket, pension, spouse’s income, and state taxes, I’m happy to walk through it with you.

This article is for general educational purposes and reflects the situation of a typical career service member under the legacy High-3 retirement system; it is not individualized tax, legal, or investment advice. The figures above are illustrative and rounded, use current-year brackets and IRMAA thresholds, and will differ from your own. Your bracket, your pension, your spouse’s income, and your state of residence all change the math, and tax law changes over time. Before acting, talk it through with a qualified tax professional or advisor who knows your full picture. Resilient Asset Management is a registered investment adviser; advisory services are offered only to clients under a written agreement.

Contact

502 S Main Street, Memphis, TN 38103

© 2026. All rights reserved.