Retirement Plans for the Self-Employed

Your business shouldn't be your only retirement plan. From Roth IRAs to Solo 401(k)s, self-employed workers have access to powerful tax-advantaged savings tools — some with contribution limits that far exceed what traditional employees can put away.

SMALL BUSINESSRETIREMENT

Christopher Flis

3/9/20267 min read

For most workers, employers typically provide a 401(k) Plan to which employees can defer a portion of their pay with certain tax preferences. For the self-employed, the circumstances are a bit different. However, owners of their own businesses have a wide array of options available to them for retirement savings.

Note: This article provides general information related to certain types of retirement accounts. Before acting on it, consult your Tax Preparer (Accountant) and, ideally, a Financial Planner.

A note to all business owners: Choosing to work for yourself is undoubtedly a liberating experience — both from a time and creativity perspective. Financially, the typical entrepreneur usually must initially invest a considerable amount of their resources (time and money) in their fledgling company. Sooner or later, it is important for a business owner to realize that the business must also support its owner financially. Therefore, it is wise to at least consider taking money out of the business — both for salary and retirement savings — as it is easy for a business to consume all available capital. Counting on an unbelievable sale of your business is a plan, yet it is one an owner might want to hedge by taking advantage of some of the strategies described below.

Scene Setter

For the remainder of this article, let’s assume that whoever the reader is — contractor, business owner, other interested person — you are either a “1099” worker or a business owner whose company is organized as an S-Corp, LLC, or Sole Proprietorship. With this wide net of potentials, all the strategies described below are possibilities. If you are a “W-2” employee for a company you do not own, this article is not for you. Let’s also assume your business is well-financed and there is distributable cash beyond what the business needs to maintain operations.

Important: All contribution limits referenced in this article reflect 2025 IRS figures. Limits are adjusted periodically for inflation, so always confirm current limits with the IRS or your financial advisor before making contribution decisions.

Roth IRA

Established by the Tax Relief Act of 1997, the Roth IRA has a simple and powerful concept: you pay taxes now, and thereafter the funds — and any earnings on those funds — are free from tax for the remainder of the account owner’s life. There are a few key rules:

• Income Limit: $161,000 for single filers; $240,000 for married filers (2025)

• Maximum Contribution: $7,000 if under age 50; $8,000 if age 50 or older (2025)

• Contribution deadline: Contributions can be made up until the tax filing deadline — on or about April 15 of the following year

• Earned income required: You must have earned income to contribute, and may only contribute up to your earned income amount

• No age restriction: You may contribute at any age

• No Required Minimum Distributions (RMDs)

• Spousal contributions: A non-working spouse can open a Roth IRA based on the working spouse’s earnings

• Inherited Roth IRAs: Can be passed to beneficiaries and maintain their tax-free status

• Contributions: Can be withdrawn tax-free and penalty-free at any time

• Earnings: May only be withdrawn penalty-free after reaching age 59½. Consult a tax professional regarding early withdrawal rules, including the 5-Year Rule

Practically speaking, the Roth IRA is arguably the best retirement option for the masses. The concept of paying income taxes now and never again is especially appealing if you are in a lower tax bracket. Bottom line: if you don’t have a Roth IRA, get one.

Who should use this option: For contractors or business owners looking to save up to $7,000 annually who meet the income and eligibility requirements above, this is the option for you. The paperwork is straightforward — these accounts can be opened at any reputable brokerage firm and need not be linked to your business in any way. The Roth IRA can also be used in combination with any of the strategies below, which is particularly useful if you want to maximize total retirement contributions.

SIMPLE IRA

SIMPLE stands for Savings Incentive Match Plan for Employees Individual Retirement Account. Generally speaking, this is a streamlined version of the better-known 401(k). SIMPLEs are easier and less costly to maintain than a 401(k) and are not subject to ERISA — the extensive set of regulations governing plans like 401(k)s. Key facts:

• Employer requirement: Only an eligible employer may establish a SIMPLE IRA — your entity must have its own Employer Identification Number (EIN)

• Annual contributions are not required

• 2025 contribution limit: $16,500, with catch-up contributions of $3,500 for those age 50 or older

• Withdrawals: Only permitted penalty-free at age 59½

• Rollover restriction: You cannot roll over a SIMPLE IRA to a Traditional IRA until 2 years after the SIMPLE is first funded

• Other IRAs cannot be rolled into a SIMPLE IRA

• Tax treatment: Contributions are made pre-tax, providing a current-year income tax benefit; withdrawals in retirement are taxed as ordinary income

A SIMPLE IRA functions similarly to a 401(k) but with less administrative overhead. The contribution limit of $16,500 sits between the Roth IRA ($7,000) and the Solo 401(k) ($70,000 total), making it a solid middle-ground option. The current-year tax deduction means you defer income tax now and pay it upon withdrawal in retirement — the opposite approach from a Roth.

Who should use this option: If your business can support distributions up to the $16,500 limit and you expect your income to be lower in retirement than it is today, a SIMPLE IRA may be an excellent fit. The current-year deduction is most valuable when your income — and tax rate — is at its peak. A good option for deferrals in the $7,000 to $16,500 range.

SEP-IRA

SEP stands for Simplified Employee Pension. Like the SIMPLE IRA, a SEP is not an ERISA plan and is much easier to administer than a 401(k). The IRS model form 5305-SEP provides boilerplate language for establishing the plan — most reputable brokerage firms will have the necessary documents. Key SEP specifics:

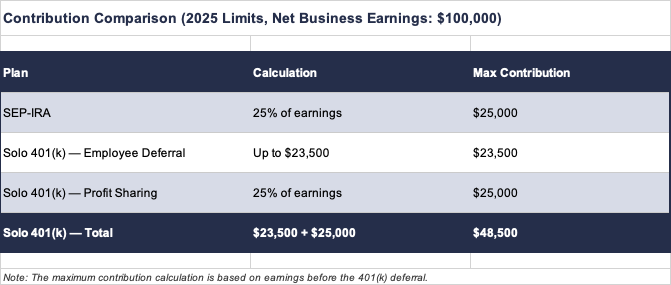

• Contribution limit: Up to 25% of compensation, with a maximum of $70,000 (2025)

• Self-employed calculation: For sole proprietors, the contribution limit is based on Schedule C income; for partnerships, your K-1 determines the limit

• EIN required: You will need an Employer Identification Number for your business

• Contributions are discretionary — you are not required to contribute every year

• Tax treatment: You receive a current-year tax deduction; there are no Roth SEPs

• Withdrawals: Subject to the same rules as traditional IRAs — penalty-free after age 59½, taxed as ordinary income

Who should use this option: If you have substantial business income and the capacity to make sizable retirement contributions, the SEP-IRA is an excellent choice. The discretionary nature of contributions also makes it well-suited to businesses with variable income — strong years you contribute generously, lean years you skip it. All in all, this is a great option for the self-employed.

Individual 401(k) — The Solo 401(k)

Also referred to as the “Solo 401(k),” the Individual 401(k) is similar in form and structure to the employer-provided 401(k) most people are familiar with. Your business must have its own EIN. To establish the plan, you complete a plan document — typically a boilerplate form provided by the brokerage firm you select as Trustee — and then open your individual account within it.

The Solo 401(k) is similar in nature to the SEP-IRA but with a key advantage: higher potential contribution limits. Here’s how it works:

• Employee deferral: You can contribute up to $23,500 of W-2 or self-employment income (2025)

• Profit sharing: In addition to the employee deferral, you can make a “profit sharing” contribution of up to 25% of W-2 income or 20% of net self-employment income

• Total limit: Combined contributions cannot exceed $70,000 (2025), or $77,500 with catch-up contributions if age 50 or older

• IRA independence: Contributions to a Solo 401(k) are independent of any IRA contributions — so you can still contribute to a Roth IRA alongside this plan

• Spouse: You may establish an account for your spouse if they are employed within the business

• Form 5500: Once plan assets exceed $250,000, you must file Form 5500 annually — a relatively straightforward process your plan Trustee will support

• Rollovers: Depending on your provider, you can roll in funds from other 401(k)s and/or Traditional IRAs, which may also enable future Backdoor Roth contributions (consult your tax advisor)

• Loans: Some Trustees permit 401(k) loans. While borrowing against retirement funds is generally not advisable, self-employed individuals may find this flexibility valuable for business opportunities

• Future employees: The Solo 401(k) is designed for individuals. If you anticipate hiring employees in the future, this plan may not be the right long-term fit

Roth Solo 401(k)

The SECURE 2.0 Act (2022) expanded and clarified Roth options within Solo 401(k) plans, and today most major brokerage firms — including Vanguard, Fidelity, and Schwab — offer Roth Solo 401(k) accounts. This means you can now defer up to $23,500 into a Roth Solo 401(k), where contributions grow tax-free. Depending on your tax situation and long-term goals, the Roth option may be highly advantageous — particularly for those who expect higher tax rates in retirement or who are building a legacy for heirs.

Who should use this option: This is an ideal plan for high-income earners. More specifically, if you earn a significant amount from a secondary income source, this plan makes a great deal of sense. Consider a long-tenured Military Retiree — say a 26-year O-6:

• Her annual pension may approach $85,000.

• VA Disability, if applicable, may add another $1,000 or more per month — tax-free.

• Combined, just from military benefits, this retiree may clear close to $100,000 annually, with highly subsidized healthcare.

• With an empty nest, a paid-off mortgage, and a reasonable budget, she may have little need for additional earnings.

• If she also takes on consulting work earning $100,000, much of that income — if not needed for living expenses — can flow into tax-advantaged accounts, reducing her present-day tax burden significantly.

• Or, through a Roth Solo 401(k), those contributions can grow tax-free to support legacy planning.

In short, the Solo 401(k) is a powerful and often underutilized retirement planning tool with serious potential to build account balances quickly — especially when combined with Roth IRA contributions. Of all the options described here, this one offers the most flexibility and upside for the right candidate.

Conclusion

Regardless of which option you choose, once your plan is established and your account is open, contributions will flow in and you will have an exceptionally wide array of investment choices available to you — far more than the typical employer-provided 401(k). And since investment expenses continue to trend lower, you can build a diversified portfolio with rock-bottom fees.

Being self-employed does not mean being without retirement savings opportunities. In fact, you have more options available to you than most employees do. Once your business is established and generating consistent cash flow, you should factor these strategies into your financial planning. A financial planner, working in concert with your accountant, can help you identify the best plan for your specific situation.

If you have any questions about any of the retirement strategies mentioned in this article, please feel free to reach out to us at Resilient Asset Management.

Contact

502 S Main Street, Memphis, TN 38103

© 2026. All rights reserved.